People's Bank Reports First Quarter Earnings

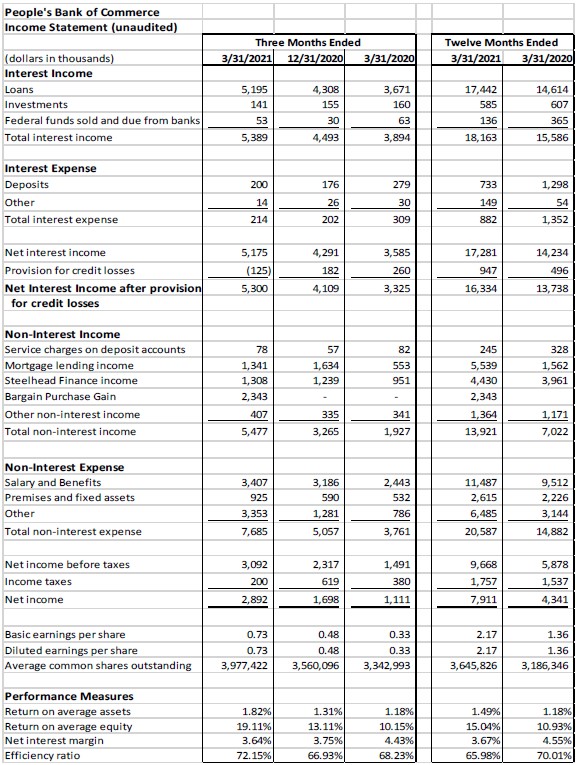

Medford, Oregon - People’s Bank of Commerce (OTCBB: PBCO) announced today its financial results for the first quarter of 2021. The bank reported net income of $2,892,000, or $0.73 per diluted share, for the first quarter of 2021 compared to net income of $1,111,000, or $0.33 per diluted share, in the same quarter of 2020. First quarter earnings in 2021 were impacted by the one-time, non-recurring merger accounting adjustments with Willamette Community Bank totaling $527 thousand or $0.10 per diluted share. Earnings per share for the trailing 12 months were $2.17 per share up from $1.36 per share for the same period of 2020, or a 59% increase.

The first quarter of 2021 reports consolidated numbers after the merger and are compared to PBCO on a standalone basis for the first quarter of 2020:

- Total assets of $808 million, an increase 116%, compared to the first quarter of 2020

- Net loans of $508 million, an increase of 91% compared to the first quarter of 2020

- Deposits of $719 million, an increase of 132% compared to first quarter of 2020

- Tangible book value per share of $14.13, an increase of 15% compared to first quarter of 2020

Acquisition of Willamette Community Bank

On March 1, 2021, the bank completed the acquisition of Willamette Community Bank (“WMCB”). As of the acquisition date, WMCB was merged with and into People’s Bank of Commerce.

As a result of the merger agreement, WMCB shareholders received 0.6665 shares of People’s Bank common stock plus $1.70 in cash per share for each share of WMCB common stock. People’s Bank issued an aggregate 1,238,334 shares of its common stock and paid cash of $3.2 million for total consideration paid of $20.4 million.

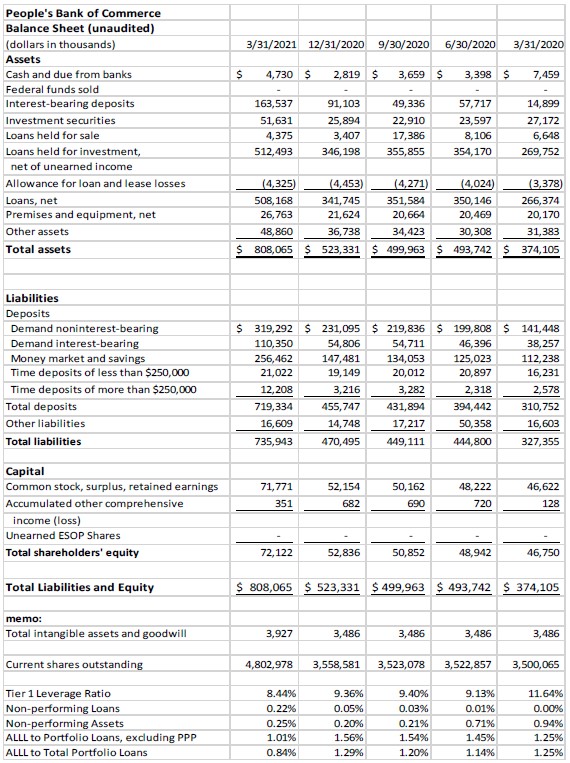

Balance Sheet

The bank’s total assets increased $284.7 million, or 54%, to $808.1 million at March 31, 2021, from $523.3 million as of December 31, 2020. The WMCB merger resulted in an increase of total assets, $221.6 million at the merger date.

Investment securities increased $25.7 million, or 99.4%, during the quarter to $51.6 million as of March 31, 2021 from $25.9 million as of December 31, 2020. The increase was primarily the result of investments acquired in the WMCB merger, which the bank has retained within its portfolio.

Total portfolio loans, net of allowance for loan losses, increased $166.4 million, or 48.7%, to $508.2 million as of March 31, 2021, versus $341.7 million at December 31, 2020. Total loans outstanding, excluding loans acquired in the WMCB merger, increased $22.3 million during the quarter.

Total deposits increased $263.6 million, or 57.8%, to $719.3 million as of March 31, 2021 from $455.7 million at December 31, 2020. Of the increase, $197.9 million was attributed to the WMCB merger. The bank completed a one-way sell of $19.5 million in one-month CDARS during the quarter. This sell was designed to reduce the already high liquidity position of the bank.

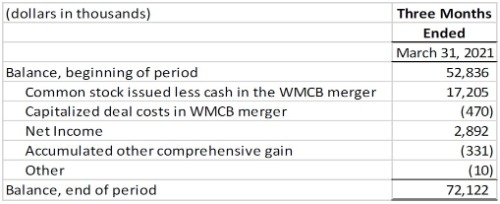

Total shareholders’ equity increased $19.3 million, or 36.5%, during the quarter. Changes in equity during the three months ended March 31, 2021 were as follows:

Operating Results

Net income increased $1,781,000, or 160%, to $2,892,000 through March 31, 2021 versus the first quarter of 2020.

During the first quarter of 2021, interest income and fee amortization of PPP loans resulted in additional interest income of $1.4 million.

Non-interest income increased by $3,550,000, or 184.2%, versus the same quarter prior year. The increase was attributed to an increase in mortgage lending income of $788 thousand, or 143%, to $1,341,000 through March 31, 2021, and an increase in Steelhead Finance factoring income of $357 thousand, or 38%, to $1,308,000 for the current quarter versus the prior year. In addition, there was a bargain purchase gain of $2,343,000 from the WMCB merger.

Non-interest expense for the first quarter of 2021 was $7.7 million compared to $3.8 million for the same quarter of 2020, significantly impacted by the one-time merger expenses of $2.9 million. Deducting the one-time non-interest expenses associated with the merger of $2.9 million results in core expenses of $4.8 million in the first quarter of 2021, a 28% increase over the prior year. During the first quarter 2021, $361 thousand in PPP fee income was applied as an offset to employee expense for processing of new PPP loans added during the quarter. In addition, the bank has committed to provide $1 million in intermediate and long-term housing relief in Southern Oregon from fires experienced in our community in 2020, of which $250 thousand was expensed in the first quarter of 2021.

The one-time merger expenses in the first quarter of 2021 resulted from the following:

Data processing conversion & termination fees: $ 1,801,000

Personnel – Change in control and severance payments: 638,000

IT support and maintenance: 283,000

Legal expense: 73,000

Professional expense: 40,000

Shareholder expense: 35,000

Total $2,870,000

Excluding one-time merger adjustments, diluted earnings per share would have been $0.83 for the quarter ended March 31, 2021, versus $0.33 for the same quarter, prior year. For the twelve months ended March 31, 2021, excluding one-time merger expenses, earnings per share would have been $2.28 as of March 31, 2021, versus $1.36 for the same twelve month’s ended March 31, 2020.

CEO’s Comments

“With the merger of Willamette completed on March 1st, all anticipated merger expenses have been expensed in the first quarter,” commented Ken Trautman, CEO. “These merger expenses were offset by strong earnings during the quarter, including performance from our factoring company, Steelhead Finance, and from the mortgage division. Steelhead and mortgage combined reported gross income for the current quarter of $2,649,000 vs. $1,504,000 for the same period in 2020, a 76% increase.”

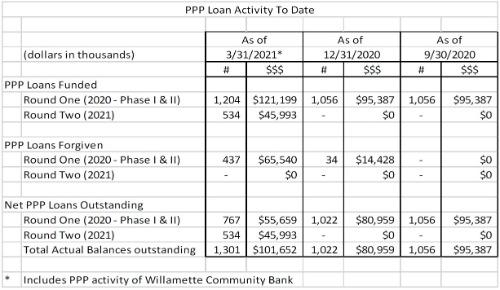

“The loan pipeline for the combined bank continues to be strong with approved credits pending funding totaling $65.3 million as the March 31, 2021. PPP loans outstanding as of quarter end were $102 million, with year-to-date PPP loan fee income of $1.5 million. The balance of the PPP loan fee income expected to be earned in 2021 totals $3.1 million,” commented Trautman.

“The bank worked very hard to respond to the needs within our communities during the Covid pandemic. It was a monumental, unified effort across all departments within the bank to deliver the volume of PPP loans we did and to have had the resulting positive impact on our local economies. Our staff continues to work very hard in providing new Round 2 PPP loans and in facilitating our clients' receipt of forgiveness,” noted Trautman. The table below presents the number and dollar amounts of the bank's PPP activity to date by quarter:

Credit Quality & Provision for Credit Losses

Loan quality continues to be strong with 0.22% of loans past due over 30 days or on Non-Accrual at the end of the first quarter of 2021 vs. 0.00% for the same period last year. There were four loans on deferral as of March 31, 2021, with outstanding balances of $3.5 million. Of the deferred loans, two are hospitality loans with outstanding balances of $988 thousand, one loan to a faith-based organization has an outstanding balance of $2 million, and one loan to a national social/service organization has an outstanding balance of $532 thousand.

Now that the bank has a better feel for the effect of COVID in our markets, the bank decreased its reserve to outstanding loans, (excluding PPP loans) to 1.01% at the end of the first quarter in 2021. The Allowance for Loan and Lease losses (ALLL) was reduced 1.45% for People’s Bank portfolio loans and all Willamette Community Bank (WMCB) new loans booked in March of 2021, excluding PPP. The ALLL for WMCB was eliminated at the completion of the merger and a fair value adjustment was applied to the outstanding portfolio per GAAP purchase accounting guidelines. The carrying value of the loans acquired in the WMCB merger was $145.5 million and the related fair value discount was $1.2 million or 0.84% of the acquired balance. The unallocated portion of the reserve stands at $964 thousand or 22.3% of the ALLL.

Capital

At March 31, 2021, tangible capital totaled $67.8 million. The bank’s Tier 1 Capital ratio was 8.44% at the end of the first quarter 2021, compared to 11.64% one year ago. Tangible book value per share was $14.13 on March 31, 2021, compared to $12.32 on March 31, 2020.

About People’s Bank of Commerce

People’s Bank of Commerce’s stock trades on the over-the-counter market under the symbol PBCO. Additional information about the Bank is available in the investor section of the bank’s website at: www.peoplesbank.bank.

Founded in 1998, People’s Bank of Commerce is the only locally owned and managed community bank in Southern Oregon. People’s Bank of Commerce is a full-service, commercial bank headquartered in Medford, Oregon with branches in Albany, Medford, Ashland, Central Point, Grants Pass, Klamath Falls, Lebanon, and Salem.

"Safe Harbor" Statement under the Private Securities Litigation Reform Act of 1995:

This release includes forward-looking statements intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally can be identified by phrases such as People’s Bank or its management "believes," "expects," "anticipates," "foresees," "forecasts," "estimates" or other words or phrases of similar import. Similarly, statements herein that describe People’s Bank’s business strategy, outlook, objectives, plans, intentions or goals also are forward-looking statements. All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those in forward-looking statements.