PBCO Financial Corporation Reports Q1 2023 Earnings

Medford, Oregon – PBCO Financial Corporation (OTC PINK: PBCO), the holding company (Company) of People’s Bank of Commerce (Bank), announced today its financial results for the first quarter of 2023.

Highlights

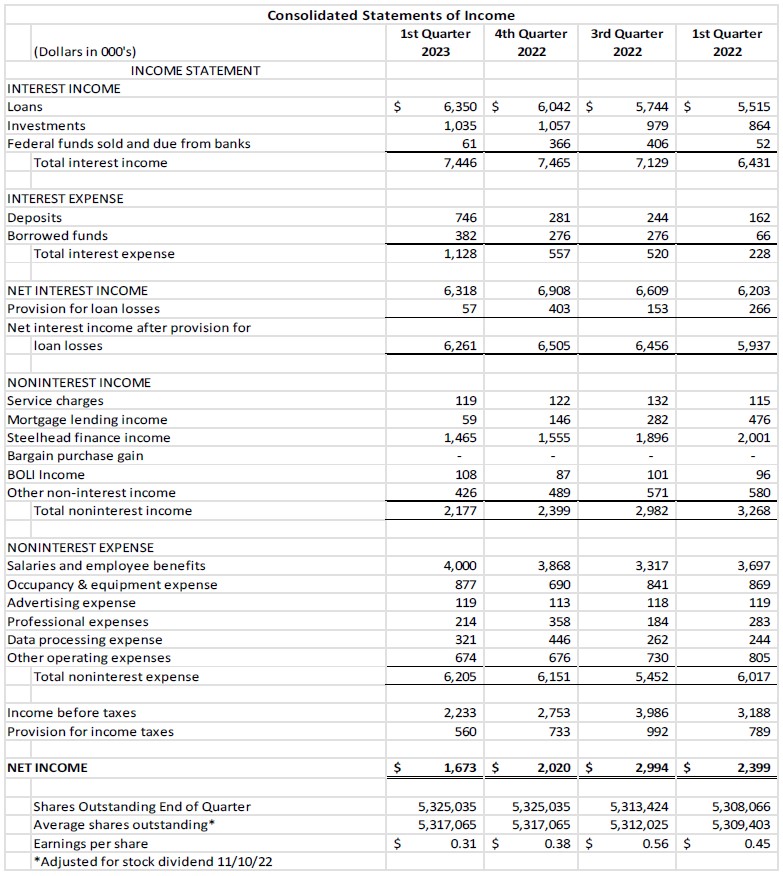

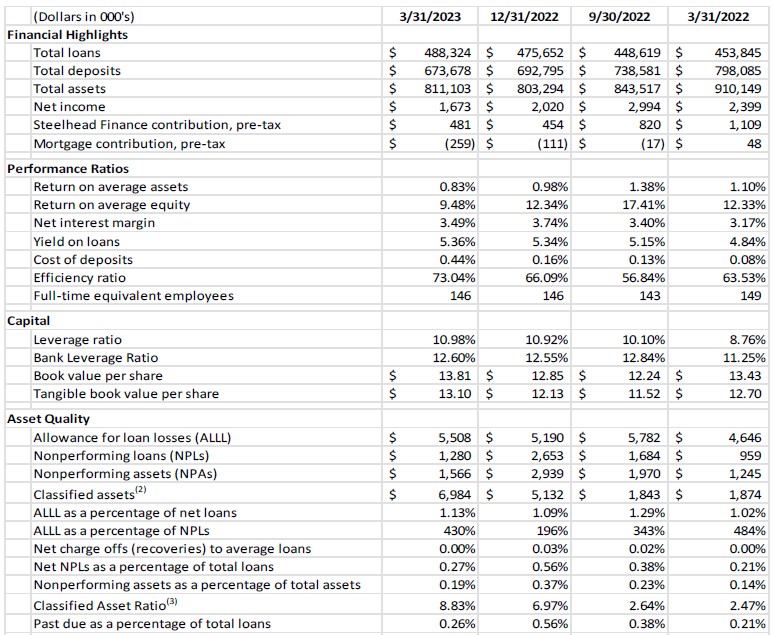

- Net income of $1.7 million in the quarter, or $0.31 per diluted share

- Loan growth of $13.0 million in the quarter, an increase of 2.74% compared to Q4 2022

- Net interest margin of 3.49%, a decrease of 0.25% compared to Q4 2022

- Cost of deposits was 44 basis points, an increase of 28 basis points when compared to Q4 2022

- Opened a full-service branch in Eugene, Oregon

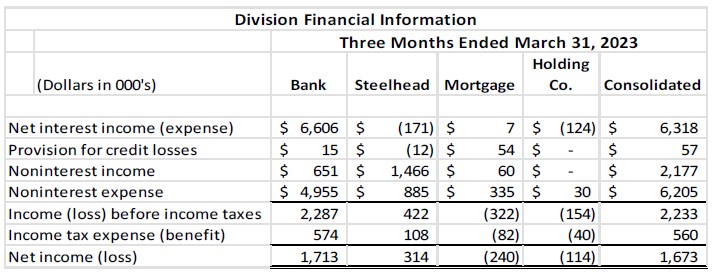

The Company reported net income of $1.7 million, or $0.31 per diluted share, for the first quarter of 2023 compared to net income of $2.4 million, or $0.45 per diluted share, in the same quarter of 2022. The reduction in earnings for the first quarter is primarily due to the rising cost of deposits as depositors sought higher yields and reduced mortgage lending and Steelhead revenue due to inflationary pressures.

“Despite higher funding costs and increased competition for deposits as liquidity left the banking system, the bank is well positioned with a strong core deposit base and capital to support future growth and economic challenges,” commented Ken Trautman, Chief Executive Officer. “The bank recently opened a new branch in Eugene as part of its strategic growth initiative,” added Trautman. “The banking industry is resilient, and in spite of recent challenges, remains strong overall versus the last economic downturn.”

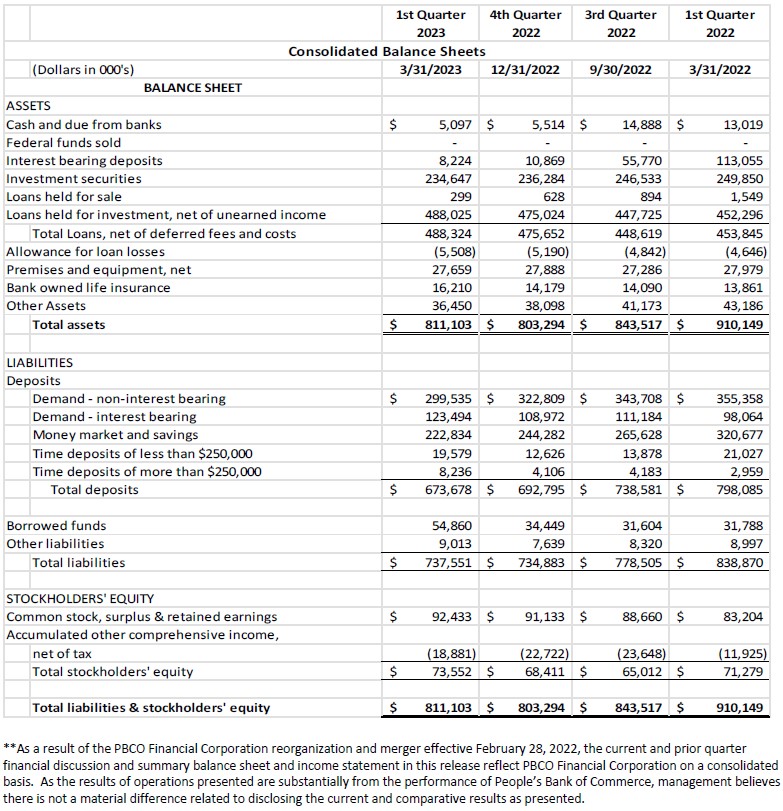

Deposits decreased $19.1 million during the quarter, a 2.8% decline from the fourth quarter of 2022. Over the last twelve months, deposits decreased $124.4 million, a decline of 15.6%. “The deposit outflow over the last year was expected considering the large deposit inflow as a result of government stimulus during the COVID-19 Pandemic,” commented Joan Reukauf, Chief Operating Officer. “Competition for deposits increased as the government began its quantitative tightening initiative in 2022, in combination with steep Fed Funds rate increases to combat persistent inflation, which incented depositors to seek higher yields on their liquid balances.”

Loans increased $13.0 million in the quarter, or 2.7% growth compared to the fourth quarter of 2022. “The bank continued to grow its loan portfolio during first quarter, with demand for loans staying strong in spite of significantly higher borrowing costs than the same period last year,” commented Julia Beattie, President.

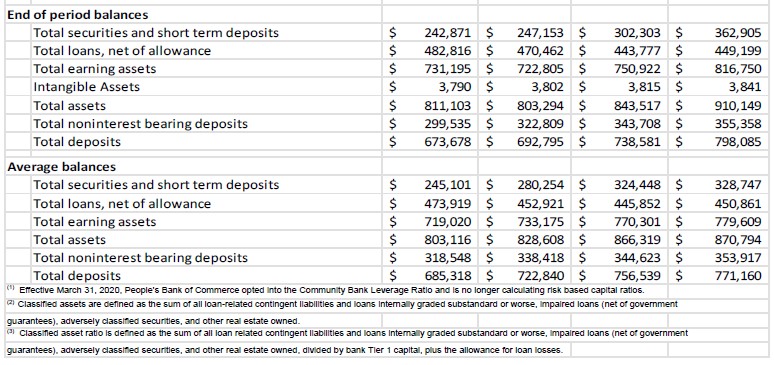

The investment portfolio decreased to $234.6 million in Q1 2023 from $236.3 million at the end of Q4 2022, a 0.7% decrease. The average life of the portfolio decreased to 4.5 years from 4.6 years during the quarter as short-term investments matured and were not replaced. Securities income was $1.04 million during the quarter, a yield of 1.76%, versus $1.06 million or a yield of 1.79% for the fourth quarter of 2022. “The bank’s investment portfolio is classified as available-for-sale, meaning there are no undisclosed, unrealized losses that could negatively impact the bank,” noted Lindsey Trautman, Chief Financial Officer. “While rising interest rates have negatively impacted the market value of our investment portfolio, the bank continues to be well-capitalized when considering the impact on capital of the unrealized loss,” added Trautman. As of March 31, 2023, the net after tax unrealized loss on the investment portfolio was $18.9 million versus $22.7 million as of December 31, 2022. Highly rated government agency and government sponsored agency investments comprise 94.8% of the investment portfolio with the balance of approximately 4.5% held in municipal investments and 0.7% held in corporate sub-debt issued by community banks. As of Q1 2023, liquid assets to total assets were 24.0%, including the market value of the investment portfolio, less pledged investments of $53.7 million.

Non-performing assets improved in Q1 as total loans past due or on non-accrual decreased to 0.26%, as a percentage of total loans, versus 0.56% as of Q4 2022. “Credit quality has remained strong during the first quarter, with past due loans improving from the prior quarter,” noted Bill Whalen, Chief Credit Officer. During the first quarter, the Allowance for Loan and Lease Losses (ALLL) increased by $318 thousand. Of the increase, $261 thousand was attributed to implementation of the new Current Expected Credit Losses (CECL) accounting standard, which went into effect on January 1st and provides for an accounting adjustment as an offset to retained earnings, net of deferred taxes. The difference of $57 thousand was the loan loss provision for the quarter under the new standard. As of March 31, 2023, the ALLL was 1.13% of portfolio loans.

First quarter 2023 non-interest income totaled $2.2 million, a decrease of $222 thousand from the fourth quarter of 2022. During Q1 2023, Steelhead Finance factoring revenue decreased $90 thousand, a 5.8% decrease from the prior quarter. “Although factoring revenue decreased during the 2nd half of 2022 and Q1 of 2023, overall activity is strong and will continue to provide a diversified income source outside of the bank’s traditional banking products” commented Bill Stewart, President of Steelhead Finance. Increased mortgage rates have continued to negatively impact mortgage production, and consequently, mortgage income decreased $87 thousand, or 59.6%, from the fourth quarter of 2022. “Although mortgage production continued to trend negatively during the first quarter, mortgage rates have improved recently,” commented Echo Hutto, the mortgage division manager. “The bank recently hired a new team of seasoned mortgage lenders to increase production in our northern market going into the spring and summer months,” added Hutto.

Non-interest expenses totaled $6.2 million in the first quarter, up $54 thousand from the previous quarter. The primary reason for the increase in expenses was attributed to salary adjustments implemented at the start of the year. “The bank has focused on improving efficiency in 2023 as a strategic objective for the year,” noted Beattie. “The board and management have set a goal to be more efficient as the bank matures into its existing infrastructure. The Eugene expansion and the recent increase in the mortgage lending team will have a short-term impact on efficiency that should correct as we penetrate new markets,” added Beattie.

As of March 31, 2023, the Tier 1 Capital Ratio for PBCO Financial Corporation was 10.98% with total shareholder equity of $73.6 million. During the quarter, the Company was able to augment capital through earnings, while the unrealized loss on the investment portfolio also improved, as noted above. The Tier 1 Capital Ratio for the Bank was 12.60% at quarter-end, up from 12.55% as of December 31, 2022. Tangible Capital was $69.8 million, or 8.60% as of March 31, 2023, versus Q4 2022 at $64.6 million or 8.04%.

About PBCO Financial Corporation

PBCO Financial Corporation’s stock trades on the over-the-counter market under the symbol PBCO. Additional information about the Company is available in the investor section of the Company’s website.

Founded in 1998, People’s Bank of Commerce is a full-service, commercial bank headquartered in Medford, Oregon with branches in Albany, Ashland, Central Point, Eugene, Grants Pass, Jacksonville, Klamath Falls, Lebanon, Medford, and Salem.

"Safe Harbor" Statement under the Private Securities Litigation Reform Act of 1995:

This release includes forward-looking statements intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally can be identified by phrases such as People’s Bank or its management "believes," "expects," "anticipates," "foresees," "forecasts," "estimates" or other words or phrases of similar import. Similarly, statements herein that describe People’s Bank’s business strategy, outlook, objectives, plans, intentions or goals also are forward-looking statements. All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those in forward-looking statements.