PBCO Financial Corporation Reports Q2 2022 Earnings

Medford, Oregon – PBCO Financial Corporation (OTC PINK: PBCO), the holding company of People’s Bank of Commerce, announced today its financial results for the 2nd quarter 2022. As a result of the PBCO Financial Corporation reorganization and merger effective February 28, 2022, the current period financial discussion and summary balance sheet and income statement in this release reflect PBCO Financial Corporation on a consolidated basis, while the comparative prior periods are People’s Bank of Commerce results only. As the results of operations presented are substantially from the performance of People’s Bank of Commerce, management believes there is not a material difference related to disclosing the current and comparative results as presented.

Highlights

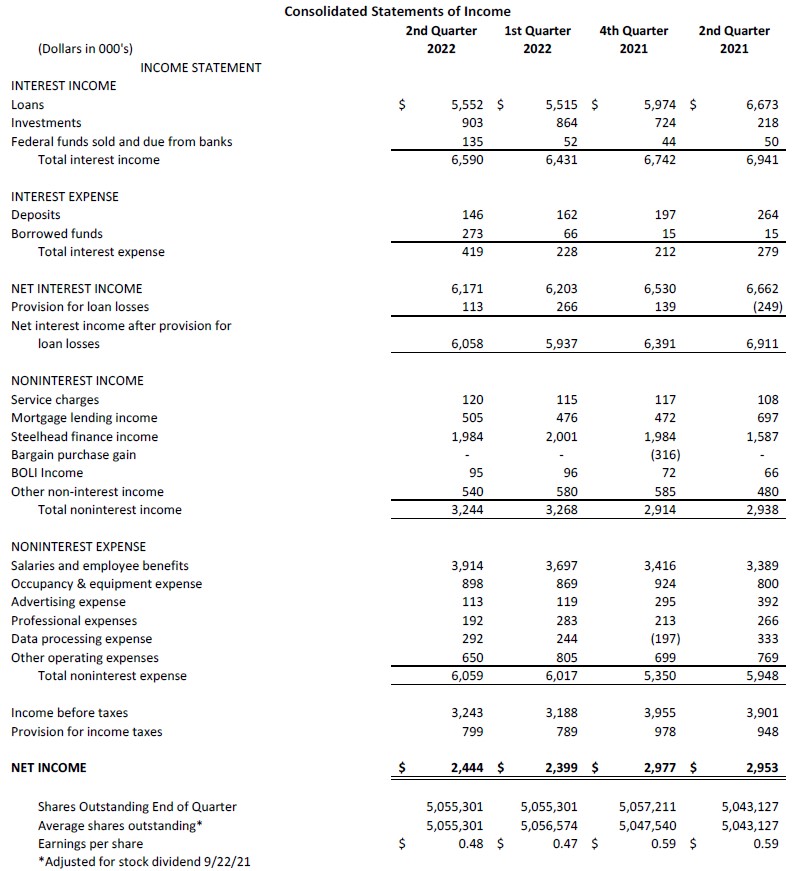

- Second quarter net income of $2.4 million, or $0.48 per diluted share

- Steelhead gross factoring revenue of $2.0 million, an increase of 25.0% from Q2 2021

- Core earnings (excluding PPP fee income) up 25.9% from Q2 2021

- Investment securities increased $140.7 million, or 135.1%, over Q2 2021

The company reported quarterly net income of $2.4 million, or $0.48 per diluted share, for the 2nd quarter of 2022 compared to net income of $3.0 million, or $0.59 per diluted share, in the same quarter of 2021. Earnings per share for the trailing 12 months were $2.08 per share, down from $2.28 per share for the prior twelve-month period. “Although earnings were impacted by the absence of income from PPP, the bank performed according to expectations during 2nd quarter. Excluding PPP income for the 2nd quarter of 2021, EPS would have been $0.38 per share, demonstrating the strength in core earnings for the most recent quarter,” said Lindsey Trautman, Chief Financial Officer. During the quarter, the company also made a provision for loan losses of $113 thousand. “The second quarter of 2022 represents the first time in two years that earnings are not materially impacted by PPP loans or merger related adjustments and more closely represent core bank earnings going forward,” commented Ms. Trautman.

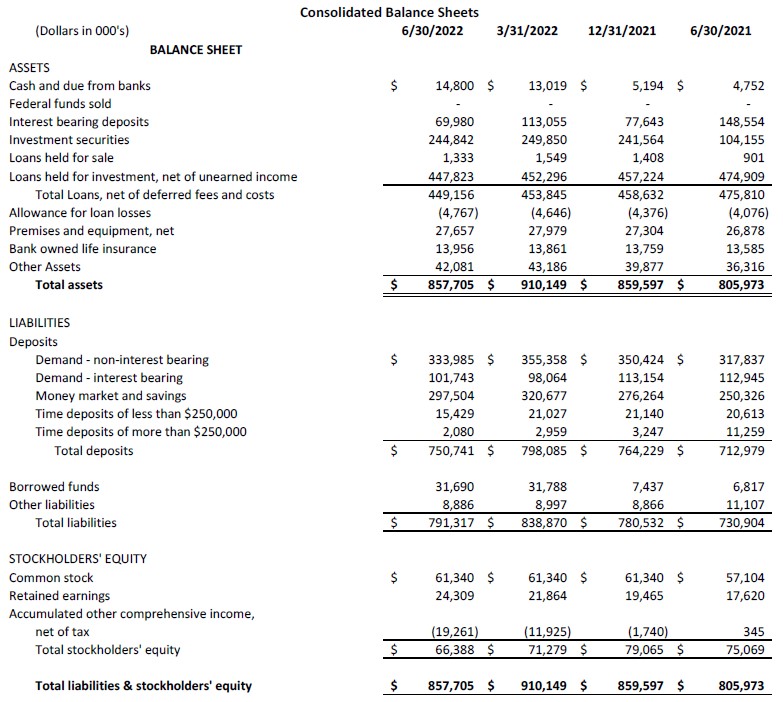

Deposits decreased $47.3 million, a 5.9% decrease from the prior quarter ending March 31, 2022. Over the last 12 months, deposits grew by $37.8 million, an annualized 5.3% growth rate. “During 2nd quarter, the company experienced a decrease in deposits, primarily related to tax payments made in April after ramping up in March,” commented Joan Reukauf, Chief Operating Officer.

“Portfolio loans were down $4.5 million during the 2nd quarter of 2022, compared to 1st quarter of 2022,” commented Julia Beattie, President. “During 1st quarter, the bank experienced strong competition for long-term fixed rate loans which materialized into continued downward pressure during the 2nd quarter. This competition has eased with the rising rate environment but impacted 2nd quarter loan growth overall,” added Beattie. The last four remaining PPP loans were forgiven during 2nd quarter.

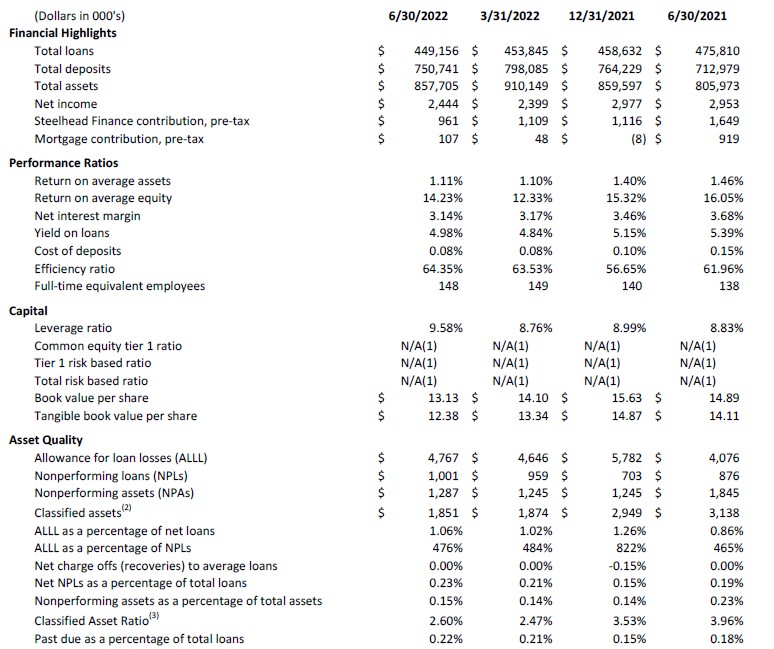

Classified assets were flat from the prior quarter in both Other Real Estate Owned and classified loans. Total loans past due or on non-accrual increased slightly, as a percentage of total loans, from the prior quarter to 0.22% versus 0.21% as of Q1 2022. During the 2nd quarter, the Allowance for Loan and Lease Losses (ALLL) was updated based on changes in loans and updated economic expectations, which were factored into the bank’s analysis. As of June 30, 2022, the ALLL was 1.06% of portfolio loans and the unallocated reserve stood at $791 thousand or 16.6% of the allowance.

Second quarter 2022 non-interest income totaled $3.2 million, an increase of $306 thousand from the 2nd quarter of 2021. During Q2 2022, Steelhead Finance factoring revenue increased $397 thousand, a 25.0% increase over the same quarter of 2021. Conversely, mortgage income decreased $192 thousand, or 27.5%, from the 2nd quarter of 2021, due to an increase in interest rates and a softening housing market.

Non-interest expense totaled $6.1 million in the 2nd quarter, up $111 thousand from the same period in 2021. Notably, personnel expense was the largest driver for the increase in non-interest expense, up $526 thousand versus the same quarter prior year, a 15.5% increase, primarily due to increasing wage pressure in the company’s markets. Advertising expenses were down $279 thousand in the 2nd quarter of 2022 versus the same period in 2021 as the bank expensed $250 thousand in donations toward housing relief support for survivors of the 2020 Alameda Fire during 2nd quarter 2021.

As of June 30, 2022, the Tier 1 Capital Ratio for PBCO Financial Corporation was 9.58% with total shareholder equity of $66.4 million. During the quarter, the company was able to augment capital through earnings while assets also decreased with the decrease in deposits during the quarter. As of June 30, 2022, the bank’s Tier 1 Capital Ratio was 12.71%, up from 11.25% as of March 31, 2022. The company also had unrealized losses on its investment portfolio, net of taxes, of $19.3 million, which is attributed to changes in market value in the current rising rate environment. The net unrealized losses in the investment portfolio resulted in the decline in Book Value Per Share and Tangible Book Value per share from prior periods. “Losses in the investment portfolio would only be recognized if the company needed additional liquidity for operations,” commented Lindsey Trautman. “Given the company’s strong liquidity position and access to alternative sources of liquidity, the probability of recognizing any losses in the investment portfolio remains very low,” added Trautman.

“Overall, 2nd quarter of 2022 demonstrated the company’s solid core earnings and strengthened capital position which will allow us to weather the uncertain economic future,” commented Julia Beattie. “The $25.0 million sub-debt issuance completed in first quarter has allowed the company to continue implementing its strategic plan while providing a cushion, should a downturn occur,” added Beattie. “Based on experience gained in the Great Recession, we know that banks who looked to the future and planned for economic uncertainty were able to work with clients and manage through challenges as they arose, while protecting the safety and soundness of the company,” concluded Beattie.

About PBCO Financial Corporation

PBCO Financial Corporation’s stock trades on the over-the-counter market under the symbol PBCO. Additional information about the Company is available in the investor section of the Company’s website.

Founded in 1998, People’s Bank of Commerce is the only locally owned and managed community bank in Southern Oregon. People’s Bank of Commerce is a full-service, commercial bank headquartered in Medford, Oregon with branches in Albany, Medford, Ashland, Central Point, Grants Pass, Jacksonville, Klamath Falls, Lebanon, and Salem.

"Safe Harbor" Statement under the Private Securities Litigation Reform Act of 1995:

This release includes forward-looking statements intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally can be identified by phrases such as People’s Bank or its management "believes," "expects," "anticipates," "foresees," "forecasts," "estimates" or other words or phrases of similar import. Similarly, statements herein that describe People’s Bank’s business strategy, outlook, objectives, plans, intentions or goals also are forward-looking statements. All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those in forward-looking statements.