PBCO Financial Corporation Reports Q4 and 2023 Earnings

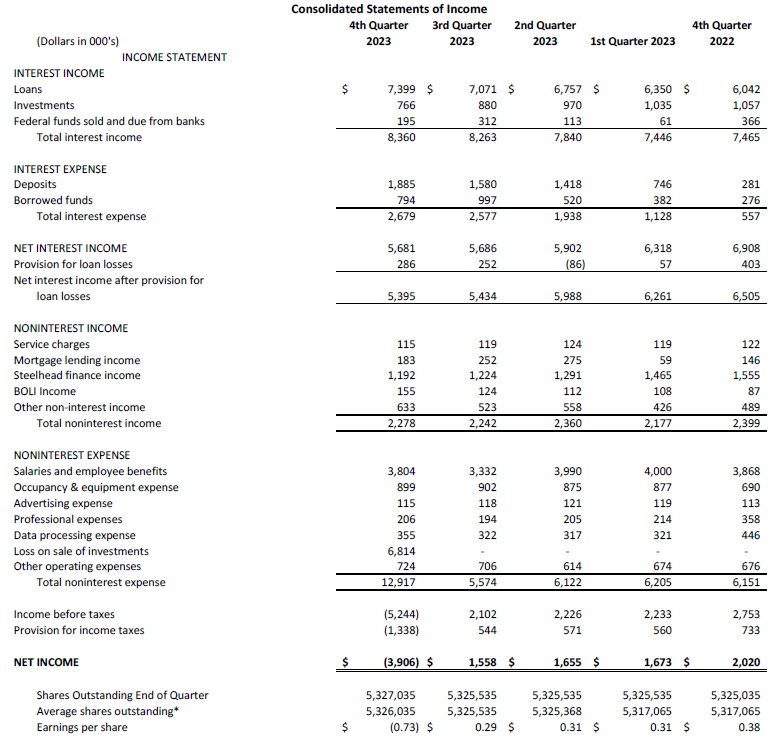

Medford, Oregon – January 24, 2024 - PBCO Financial Corporation (OTCPK: “PBCO”), the holding company (Company) of People’s Bank of Commerce (Bank), today reported a loss of $3.90 million and earnings per diluted share of -$0.73 for the quarter ended December 31, 2023, compared to earnings of $1.56 million and $0.29 per diluted share for the quarter ended September 30, 2023. For the full year, the Company posted net income of $0.99 million or $0.19 per diluted share compared to $9.86 million for 2022 or $1.92 per diluted share.

Highlights

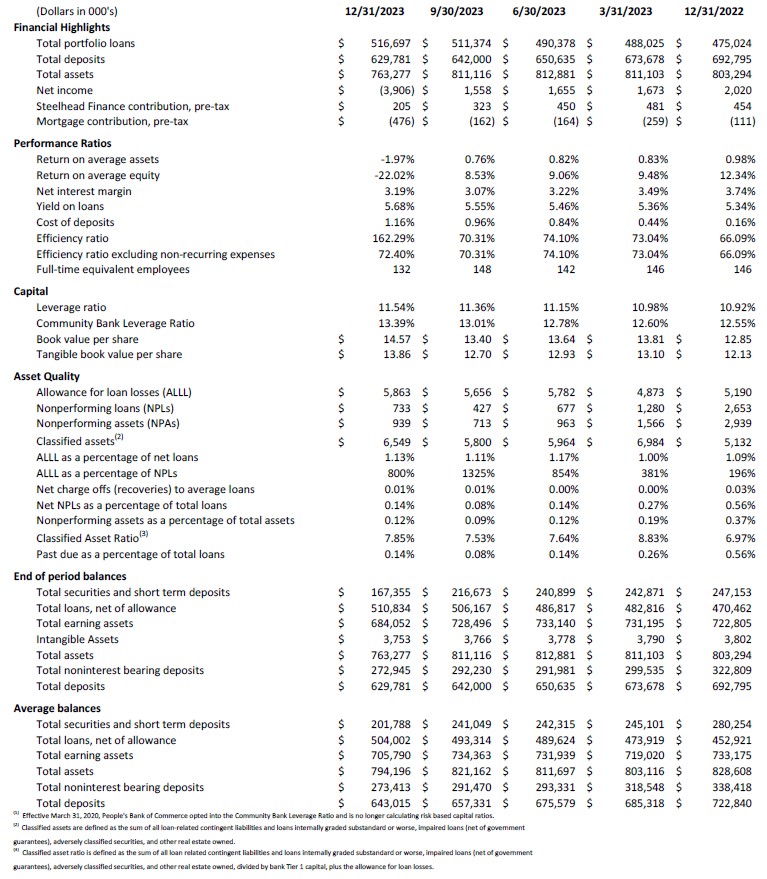

- Net interest margin increased to 3.19%, compared to 3.07% in the prior quarter

- Tangible book value per share increased to $13.86, compared to $12.70 in the prior quarter

- Loan portfolio increased by 8.8% compared to year-end 2022

- Recognized pre-tax loss of $6.8 million on sale of $49.4 million of investment securities

- Exited residential mortgage lending

The Company made two notable, strategic business decisions in the fourth quarter of 2023. The first initiative was the closure of the residential lending division as of November 1, 2023, due to industry trends and the challenging outlook for residential loan demand in 2024 and beyond. The closure resulted in one-time expenses of $340 thousand. The second was the sale of $49.4 million of investment securities at a pre-tax loss of $6.8 million. “These decisions were made to improve the Company’s future profitability and strengthen our balance sheet. We were able to execute both of these initiatives due to our strong capital position,” commented Julia Beattie, President & CEO.

Excluding the loss on sale of securities and one-time cost from exiting the mortgage business, net income was $1.4 million, or $0.27 per diluted share in fourth quarter of 2023, and $6.3 million, or $1.18 per share for the year ended December 31, 2023.

“We remain focused on maintaining our core deposit franchise and strong credit culture, while serving our communities and supporting our clients,” added Beattie. Credit quality remained strong with non-performing assets slightly higher at 0.12% of total assets, versus 0.09% in the third quarter 2023, but still low compared to the company’s historical performance.

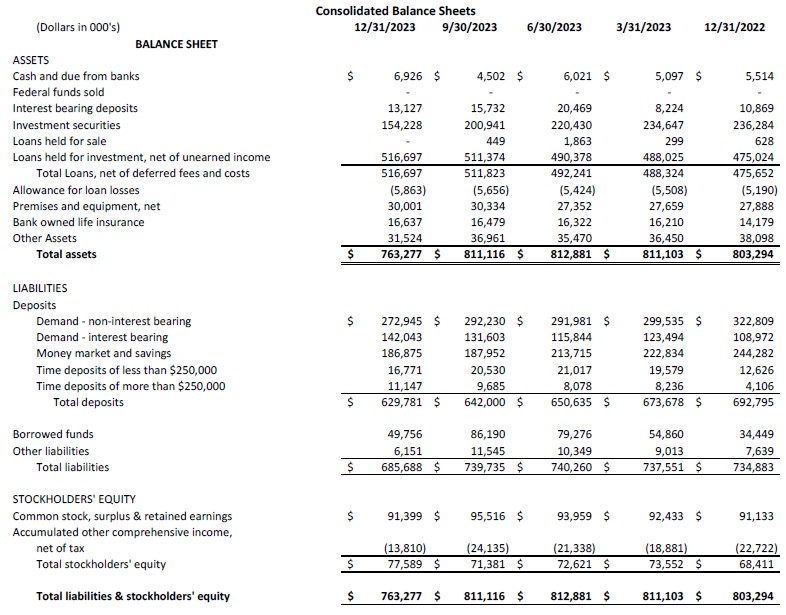

The investment portfolio decreased 23.3% to $154.2 million in the fourth quarter of 2023 from $200.9 million at the end of the third quarter 2023. The decrease was driven primarily by the sale of $49.4 million in investments during the quarter. The average life of the portfolio was 4.2 years at the end of the fourth quarter, versus 4.5 years at the prior quarter-end. Securities income was $0.77 million during the quarter, a yield of 1.67%, versus $0.88 million, and a yield of 1.66% for the third quarter of 2023. As of December 31, 2023, the net after tax unrealized loss on the investment portfolio decreased to $13.8 million versus $24.1 million as of September 30, 2023. The improvement was partly due to the loss recognized with the sale of investments in December, but also improved due to the decrease in market rates at year-end. Highly rated government agency and government sponsored agency investments comprise 95.9% of the investment portfolio with the balance of approximately 2.9% held in municipal investments and 1.2% held in corporate sub-debt issued by community banks. As of the fourth quarter 2023, liquid assets to total assets were 13.6%, including the market value of the investment portfolio less pledged investments.

Deposits decreased $12.2 million during the quarter, a 1.9% decline from the third quarter of 2023. For the year, deposits decreased $63.0 million, a 9.1% decrease from 2022. “The pace of deposit runoff slowed substantially during the 2nd half of the year,” commented Beattie.

Fourth quarter 2023 non-interest income totaled $2.3 million, an increase of $36 thousand from the third quarter of 2023. The increase was primarily attributed to a large prepayment penalty of $174 thousand collected on an early loan payoff. Steelhead revenue was down $32 thousand from the prior quarter, a 2.6% decrease. “While still a strong revenue source, our factoring division has experienced the effects of a negative year-over-year trend in the transportation industry,” noted Beattie. Mortgage revenue was down $69 thousand in the quarter with the closure of the Division effective November 1st. For the year, non-interest income was $9.1 million, a decrease of $2.8 million, or 23.8% from 2022. Steelhead revenue was $5.2 million, a decrease of $2.3 million from 2022, or a 30.5% reduction. Mortgage revenue was $769 thousand for the year, down $639 thousand from 2022, or a 45.4% decrease from prior year.

Non-interest expenses totaled $12.9 million in the fourth quarter, up $7.3 million from the previous quarter. Of the increase, $6.8 million represents the loss on sale of investments and $340 thousand was related to the exit of residential mortgage lending. This one-time expense is reflected in both salaries and employee benefits for severance expenses, as well as data processing expense for contract terminations. The bank also wrote off $80 thousand on ORE to current estimated market value. On an annual basis, non-interest expense was $30.9 million, an increase of $7.2 million over 2022, or a 30.4% increase, directly correlated to the loss on sale of investments incurred in fourth quarter.

As of December 31, 2023, the Tier 1 Capital Ratio for PBCO Financial Corporation was 11.54% with total shareholder equity of $77.6 million, versus a Tier 1 Capital Ratio of 11.36% and total shareholder equity of $71.4 million as of September 30, 2023. The reduction in core capital during the quarter is directly attributed to the quarterly loss as the bank repositioned its balance sheet. The Tier 1 Capital Ratio for the Bank was 13.39% at year-end, up from 13.01% as of September 30, 2023. Tangible Capital was $73.8 million, or 9.73% as of December 31, 2023, versus third quarter of 2023 at $67.6 million or 8.34%, which improved due to lower market rates.

About PBCO Financial Corporation

PBCO Financial Corporation’s stock trades on the over-the-counter market under the symbol PBCO. Additional information about the Company is available in the investor section of the Company’s website.

Founded in 1998, People’s Bank of Commerce is a full-service, commercial bank headquartered in Medford, Oregon with branches in Albany, Ashland, Central Point, Eugene, Grants Pass, Jacksonville, Klamath Falls, Lebanon, Medford, and Salem.

"Safe Harbor" Statement under the Private Securities Litigation Reform Act of 1995:

This release includes forward-looking statements intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally can be identified by phrases such as People’s Bank or its management "believes," "expects," "anticipates," "foresees," "forecasts," "estimates" or other words or phrases of similar import. Similarly, statements herein that describe People’s Bank’s business strategy, outlook, objectives, plans, intentions or goals also are forward-looking statements. All such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those in forward-looking statements.